The market capitalisation of firms listed on BSE crossed $5 trillion for the primary time on Tuesday, turning the highlight on valuations.

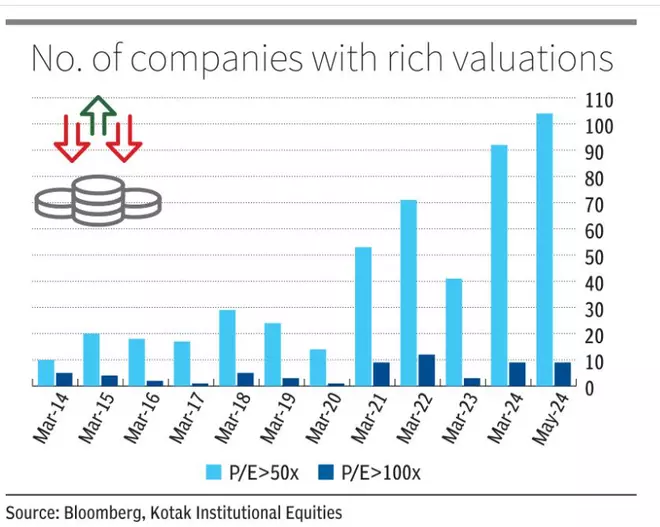

The variety of firms buying and selling at greater than 50 occasions 12-month ahead worth to earnings multiples has elevated 10x over the previous 10 years and now stands at 104 (see desk). Nifty Midcap 100 is buying and selling at 39 per cent premium to the 50-share Nifty.

The MSCI India Index has gained 35 per cent previously 12 months in contrast with 12 per cent positive factors logged by MSCI EM index, rising the premium hole over rising markets. India’s market cap to GDP ratio was at 132 per cent on the finish of April, a lot greater than the long-term common of 85 per cent.

- Learn:Bulls take BSE market-cap to new excessive of $4.03 trillion

Historic valuation

“We’re near the highest finish of the historic valuation band and the margin of security from these ranges is probably not very giant. There may be nothing low-cost out there proper now – shares are both pretty valued or overvalued,” mentioned Deepak Jasani, Head – Retail Analysis, HDFC Securities.

Public sector firms – be it banks, defence or railways – have made the transition from undervalued to pretty valued over the previous 12 months, stretching total market valuations, based on Jasani. New age companies that listed previously two years, together with firms within the digital manufacturing companies house, are costly, given their excessive market-cap and low profitability.

“A number of firms within the industrials, capital items, and defence sectors are costly, buying and selling at 80-100 PE multiples. The order e-book visibility and margins are good, however the present multiples already account for this. The margin tailwinds are over with commodity costs transferring up, and plenty of shares should not have a margin of security,” mentioned Neelesh Surana, CIO, Mirae Asset Funding Managers.

- Learn: Indices vault to new highs, BSE market cap hits ₹400-lakh crore

Jasani mentioned some huge cash had flowed in from rich traders into Indian equities previously two years and that had pushed up valuations.

“The benevolence and/or complacency of market individuals have resulted in a lot of shares buying and selling at astronomically excessive ranges. Traders could wish to get a deal with available on the market dimension implied by such excessive multiples,” mentioned a word by Kotak Institutional Equities, including that a number of excessive P/E firms are in ‘conventional’ sectors that face huge disruption dangers.

Firms require sharper and better progress charges over a shorter interval to justify excessive P/Es. A 100x P/E firm, as an illustration, might want to report an earnings CAGR of 20 per cent over the subsequent 20 years and 9 per cent CAGR over the subsequent 20.

Increased returns on playing cards

Regardless of lofty valuations, Surana believed that traders may nonetheless count on 12-15 per cent returns from a 3 to five-year horizon, given the optimistic view on the economic system and expectations of sustained momentum in earnings progress.

Based on him, a couple of non-public sector banks, the complete mass consumption sector, and pharma, notably specialty chemical compounds firms whose earnings have consolidated within the final couple of years, can be found at enticing valuations.

“Traders ought to keep away from lumpsum investments at this level however ought to make investments by SIPs in multi-cap or hybrid merchandise. Don’t chase themes equivalent to PSU, defence and manufacturing,” he mentioned.